INCREASING NUMBER OF PRICE REDUCTIONS

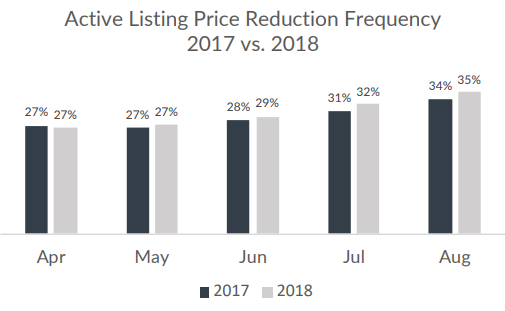

Over the past few months, there has been an increasing number of listings with price reductions. In April, 27% of Southeast Michigan active listings had at least one price reduction. By August 1st, 35% had reductions. Is this a sign that the market is shifting?

Comparing last year to this year (the dark columns represent price reduced 2017 active listings), we see the same pattern with the frequency of price reductions rising through the summer. The rising numbers are primarily seasonal. As summer progresses, sellers try harder (with price reductions) to land buyers who are looking to be settled before the start of the new school year.

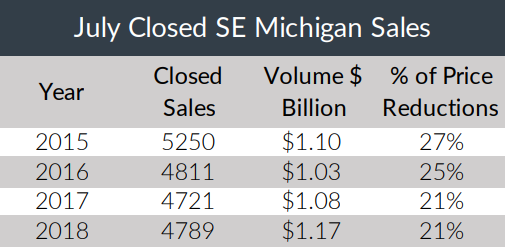

When comparing July closed sales from this year with sales from the previous three years, the Southeast Michigan markets continue to flourish. The number of closed sales was higher than last year and only down 22

DECLINING AFFORDABILITY

Real estate values have been appreciating faster than incomes for the past 7 years. Interest rates are roughly one point higher than they were a year ago. While a 1% shift in interest rate doesn’t sound like much, on a $100k home it increases the payment $58/month. That’s just the interest.

The average sale price also rose 6% over the past year. Combining the interest with price appreciation, a home that cost $100k last year will now cost $106k and will be financed at roughly 4.5% instead of 3.5%. Instead of paying $449/month (principal and interest) for that $100k house last year, this year’s payments will be $537—$88 (or 20%) higher.

Regardless of price range, by combining the rise in interest plus a 6% increase in average price, the monthly payment of the same home this year will be about 20% more than what it would have been last year. Buyers who have been struggling over the past few years to find quality homes are now faced with eroding affordability.